In this article

Looking back on Q1, the broader macro environment showed some mixed trends. While equity markets continued to soar and job growth stayed strong, inflation remained a concern, so much so that the Fed has continued to delay the originally anticipated three rate cuts this year. Despite this, the general health of the economy led to more of a risk-on appetite amongst investors which helped buoy early IPOs like Reddit and Astera Labs, hopefully encouraging other private companies to follow this quarter. Furthermore, the demand for all things AI permeated the markets and companies that were able to connect their growth story to AI trends, like Astera Labs, were well received by investors.

In the private markets, global private equity and venture deal value grew quarter-over-quarter1, though still lower than Q1 of 2023. Pre-money valuations grew for earlier stage investments and declined amongst companies post Series D, exemplifying a tougher fundraising market for later stage companies. Like in the public markets, demand for AI dominated the market. AI companies raised 17% of global funding2, a total of $11.4B in the quarter. When we zoom in to the private secondary market where EquityZen operates, we noted three private company investment trends that we’ll dive into deeper.

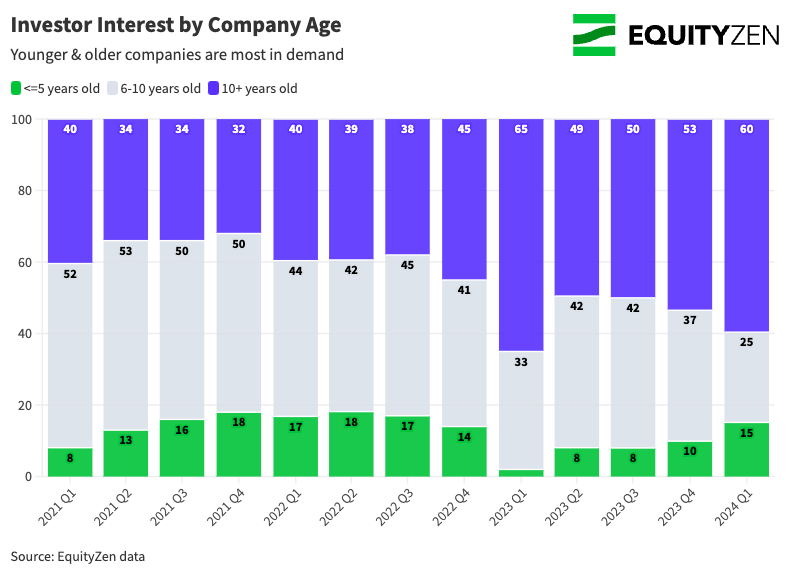

Love for the old & the young

When we look at investor demand based on company age, an interesting trend emerges. More investors are interested in both older (10+ years old) and younger (less than 5 years old) at the cost of “middle aged” private companies, as noted in the chart below. Younger companies saw an increase in investor interest, more akin to the interest we saw for companies of this age at the height of the market in 2021 and 2022. Much of this demand was driven by investor interest in AI companies. Since AI is still an emerging technology, many of these companies are inherently earlier in their lifecycle.

On the other end of the spectrum, the interest in older companies was likely driven by the expectation for more IPOs over the next several quarters. Many later stage, mature companies have both liquidity and strategic reasons to pursue an IPO and private market investors see these companies as the “IPO hopefuls” that could enter the market in the near term. Tying back to the AI trend, the most likely IPO candidates sit within the AI infrastructure and cloud space - think chips and data storage. These companies are building the infrastructure required for AI technology to be widely adopted.

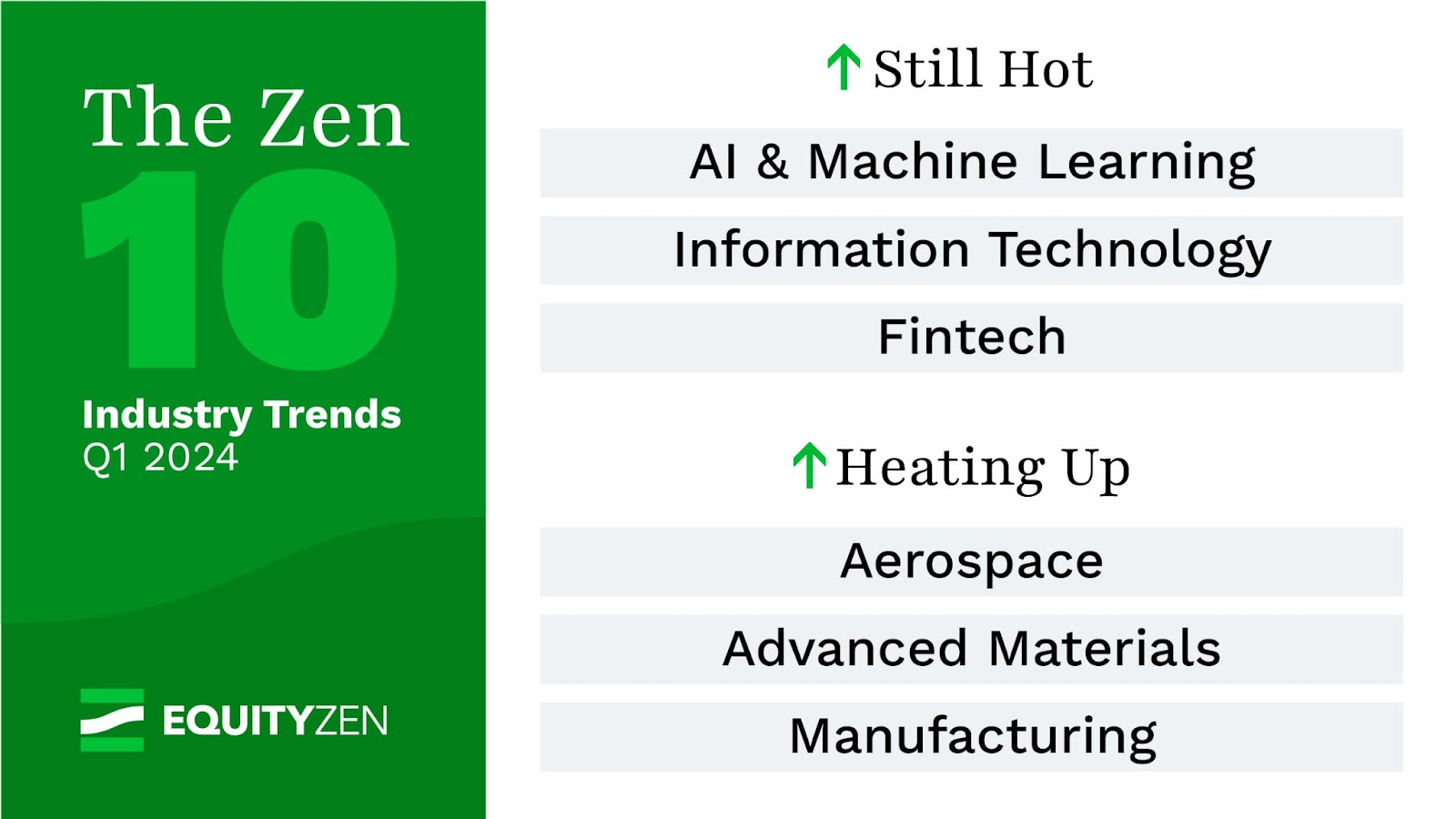

“Pure tech” remains in demand

When it came to investor interest, Q1 saw a continuation of some of the trends we saw in the back half of 2023. AI, Information Technology and Fintech reign supreme - all “pure tech” industries. Perhaps more interesting, the industries that grew in interest last quarter were focused on more tangible technologies like advanced materials and manufacturing. Private market investors are eager to be a part of the innovations happening in 3D printing, the internet of things, and supply chain automation. Meanwhile, materials like carbon composites and bioplastics have the potential for a wide range of applications from electronics to construction and aerospace, exciting investors.

Source: EquityZen data

![]()

Interested in browsing the private company investment opportunities available on EquityZen's marketplace?

A barbell mentality for valuations

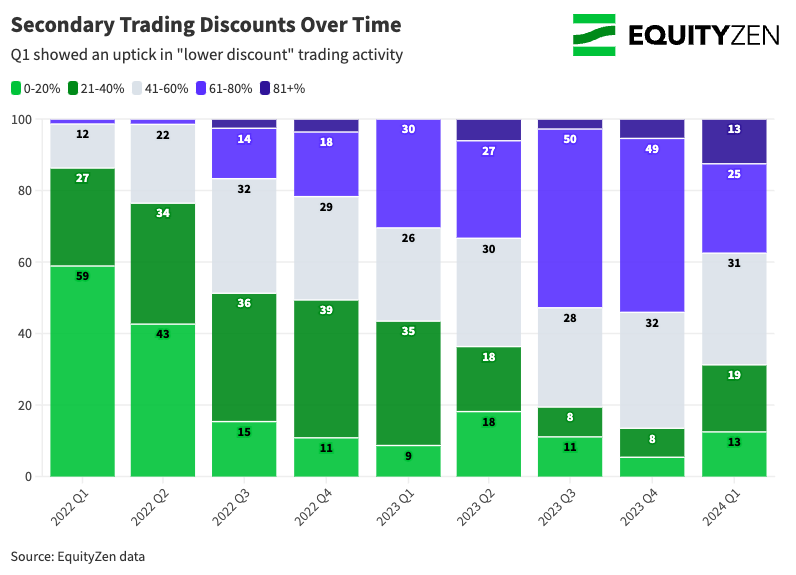

In the private secondary market, companies typically trade at a discount to their previous funding round, but this discount can vary quite significantly based on overall market factors, along with supply and demand for specific companies. The average company on EquityZen’s marketplace traded at a 28% discount to their last funding round in Q1, a marked improvement from the average discount of 40% we saw in Q4 of 20233. As investor sentiment improves and the bid-ask spread narrows, companies are trading at less aggressive discounts than we saw over the past year, a sign of normalization.

When we look at the distribution of trading discounts more closely, we see that it is not a one-size fits all story. In Q1, more companies than before (13%) traded at over an 80% discount to their last primary funding round, as noted in the chart below. These trades at such a steep discount speak to the fact investors aren’t willing to pay 2021 multiples for many companies, especially those who are not showing record growth. Meanwhile, we saw a decrease in companies trading at 40-80% and a notable increase in companies trading at lower discounts. Companies trading at less than 20% discounts can be considered the market leaders in their categories who have continued to exhibit resilience and growth, even in a tough macroeconomic and venture environment. Given these two extremes, it is a tale of two disparate trends.

While discounts are the norm in the secondary market, especially now, there are still companies trading at premiums to their last primary funding rounds. We see this most distinctly at the sector level. Industrials and Emerging Energy have both shown valuation strength, with 50% and 37% of companies respectively trading at a premium to their last round of funding. This is driven by a combination of strong individual companies, investor demand for these sectors and the likely timing of prior funding rounds, as seen in the chart below.

Meanwhile, Consumer, Lifestyle and Food & Beverage companies showed the fewest number of companies trading at a premium to their last funding round. Perhaps unsurprisingly, none of these sectors rank amongst the most popular for EquityZen investors as investor interest has shifted to more pure-technology industries.

As we move further into the year, the IPO market will continue to drive activity within the private secondary market. After all, more IPOs will provide more pricing comparables to help inform investors, ultimately enabling more primary and secondary deal activity for late stage companies. Additionally, IPOs drive liquidity that allows early investors to allocate capital to new investments. As this continues it becomes a virtuous cycle. As we watch the IPO market from the sidelines, we’ll remain active buyers in the secondary market where we see an exciting opportunity to invest in the innovators of the future.

![]()

Interested in browsing the private company investment opportunities available on EquityZen's marketplace?

Sources:

- S&P Global Private Equity Report

- Crunchbase, Q1 2024

- Source: EquityZen data

Join Investors and Shareholders Exploring the Private Markets Today