.png?width=96&height=96&name=image%20(5).png)

In this article

In the venture world, the term “exit” usually conjures images of ringing the NYSE bell or a high-priced strategic acquisition. But lately, a different kind of exit has been trending: the acquihire.

Traditionally, an acquihire allowed a larger company to pick up a startup’s engineering team and intellectual property (IP) without technically buying the company. The modern acquihire functions on a spectrum. In some cases, an asset-driven strategic hire is a “win-win” exit where healthy startups trade elite talent and IP for high-value purchase prices that satisfy both investors and employees. In other cases, the acquihire acts as a salvage mission, allowing the buyer to bypass the liquidation preferences of the startup’s investors by paying retention bonuses, dividends, or one-time distributions directly to senior leadership teams instead of a purchase amount to the company and its shareholders.

The venture capital landscape is increasingly moving toward the acquihire model as Big Tech players commit billions to secure top-tier talent. Several factors have made these high-stakes talent transfers the preferred exit strategy for today’s tech giants.

-

Scarcity of AI Talent: The global race for machine learning expertise has created a talent war where the cost of recruiting individual senior researchers often exceeds the cost of simply absorbing a specialized startup team.

-

Narrowing AI Market: As foundational models become increasingly dominated by a few massive players with the compute power to train them, smaller startups are finding it harder to compete on scale, making them more open to folding into larger ecosystems.

-

Anti-Trust Regulation: Perhaps most significantly, by structuring these deals as aggressive hiring partnerships or asset transfers rather than formal mergers, Big Tech firms may aim to bypass the oversight of anti-trust regulators who might otherwise block a full acquisition.

The Acquihire Landscape

When a deal is structured as an employment-heavy transaction, the startup’s cap table is effectively leapfrogged. Investors could be forced into a liquidity event and receive proceeds totaling their initial investment or less, while the founders and engineers walk away with lucrative pay packages.

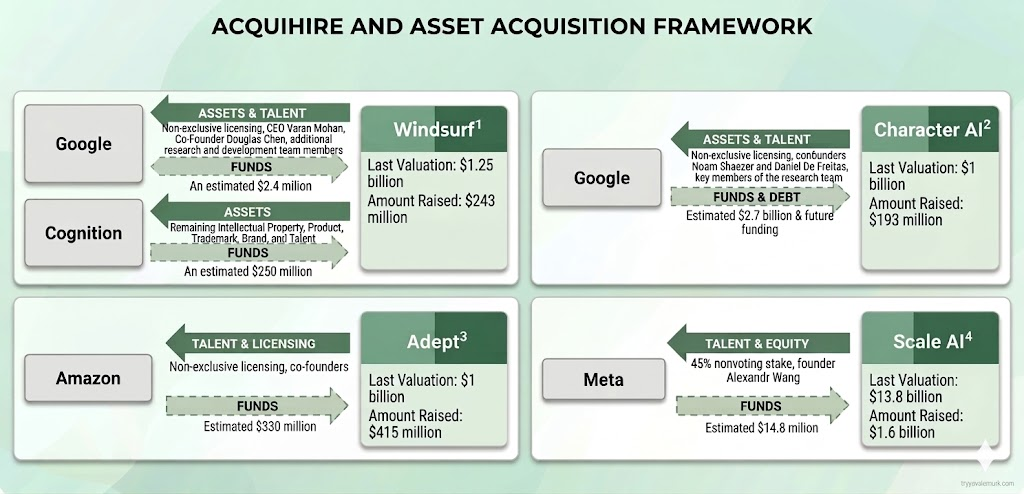

In 2024 Microsoft agreed to pay Inflection AI approximately $650 million, mostly in the form of a licensing deal. They hired most of Inflection AI’s 70-person staff, including the company’s co-founders. Inflection AI used the capital from the licensing fee to pay out the company’s existing investors with a modest return, while allowing them to maintain their equity in the remaining Inflection AI entity. This acquihire structure allowed Microsoft to avoid a lengthy review from antitrust regulators and left the prior Inflection AI entity as a shell of itself. While Inflection AI paid investors more than the value of their original investment, it ultimately forced investors into a liquidation event, bypassing their typical liquidation provisions and voting rights. Investors looking back at the deal may have preferred to have more of a say in the transaction, as we have seen the AI industry grow substantially over the last few years.

To address these shifting dynamics, institutional investors in leading private companies are increasingly moving away from handshake agreements toward legally binding charter provisions. By baking protections directly into a startup’s Certificate of Incorporation, investors are ensuring that any capital flows to company leadership or through licensing agreements adhere to shareholder voting rights and the capitalization table waterfall. This allows key investors, like VCs, to maintain some say over what exit opportunities are entertained.

We are seeing a new wave of startups, following the lead of high-profile companies adopting specific Anti-Leapfrog provisions. Here are some of the key provisions that are seeing wider adoption.

1. Broadening the Definition of a "Liquidation Event"

Traditionally, outside of an initial public offering, a liquidation event is triggered by a merger or the sale of all assets. New provisions are increasingly recognizing acquihire terms as a liquidation event, explicitly defining a Material IP License or Personnel Transfer.

- How it works: If a company licenses its core technology to a larger technology company while simultaneously transitioning its CEO and key engineering team to that buyer, it is no longer viewed as a partnership. It is legally treated as a sale.

- The Impact: When defined as a Liquidation Event in a company’s Certificate of Incorporation, transaction proceeds will flow through the company’s official liquidation waterfall, ensuring preferred shareholders are paid back in accordance with their liquidity rank. Additionally, investors are able to maintain their existing voting rights and can vote to approve the licensing deal of the Company's intellectual property, similarly to a standard liquidity event.

2. The 20% Transaction Proceeds Cap

A common tactic in recent years involves a buyer paying a small amount for a company and a massive amount in signing bonuses to the founders. Modern charters may include a Specific Stockholder Consent clause for personnel compensation.

- The Provision: Any deal where company executives or key personnel receive more than a certain percentage of the total transaction proceeds (including future employment incentives) requires a separate vote from the preferred stockholders.

- The Impact: This effectively gives investors a veto right over deals that are weighted too heavily toward executive pay at the expense of shareholder payouts.

|

Protection Mechanism |

Traditional Provision |

Modern "Acquihire Era" Provision |

|

Liquidation Trigger |

Change of Control / Asset Sale |

IP License + Mass Personnel Transfer |

|

Founder Payouts |

Often hidden in employment offers |

Capped/Subject to Investor Veto |

The Bottom Line

The changes and new provisions playing out in recent Certificates of Incorporation reflect a fundamental truth in 2026: in AI especially, talent is the asset. By anchoring the value of that talent to the capital structure, investors are ensuring that their rights are protected in acquihire situations. For private market investors, these new provisions are becoming increasingly important in protecting the return potential of private company investments.

Join Investors and Shareholders Exploring the Private Markets Today