In this article

A capitalization table also known as a “cap table” is a breakdown of a private company’s ownership structure. It displays the different securities that form the financial base of the company and the rules for each type of security. Cap tables are important when both determining a company’s valuation or pricing a private market transaction. They are also key to determining how funds from a future liquidity event would flow to various shareholders.

Typically, private companies have three liquidity or exit outcomes. The company can go public, either directly or through an initial public offering (IPO), be acquired, or ultimately fail and file for bankruptcy. Here, we will focus on the liquidation process and the waterfall of capital distributions for companies during acquisitions and IPOs.

Analyzing the Cap Table

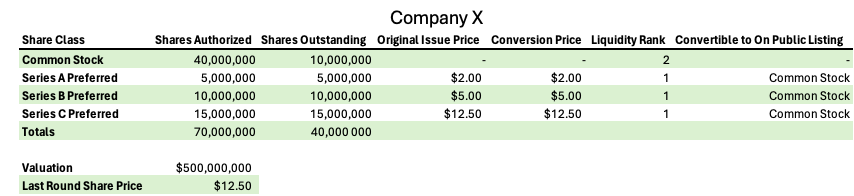

Let’s use “Company X”, with its corresponding cap table below as an example. The financial structure of Company X is broken down into one share class of common stock and three classes of preferred stock. Preferred stock is typically issued to institutional investors like venture capitalists. With Company X, preferred stock was distributed to investors to raise funding for the company with the most recent funding being the Series C round at $12.50 a share.

Investors in the preferred rounds are paid out at the same time and are the first to receive funds during a liquidity event. All three preferred rounds also have the option to convert their shares into common stock during a liquidity event unless it is a public listing, when the shares automatically convert to common stock.

Preferred shareholders can also choose not to convert their shares to common stock if the liquidation price per share of common stock is below the preferred shareholders original issue price (aka the price they paid). This is due to most preferred shareholders having at least a 1x liquidation preference. A 1x liquidation preference allows preferred shareholders to receive at a minimum the original issue price of their shares back during a liquidity event, provided that the valuation and liquidity stipulations allow for this distribution. This multiple can be higher than 1x but for the case of this example we will assume all preferred shares have a 1x liquidation multiple for Company X. The terms outlined above are relatively standard for most venture backed private companies but can differ based on the agreements between company leadership and investors in the firm.

![]()

Interested in browsing the private company investment opportunities available on EquityZen's marketplace?

When a Company is Acquired

While an IPO is thought of as the end goal for many venture capital-backed private companies, the majority of companies exit via a merger or acquisition. In fact, according to Bain Capital, more than 27,000 M&A deals completed globally in 2023 alone. This is significantly higher than the 1,429 IPOs launched globally during the same time period. Even 2021, a record year for IPOs, saw 2,682 IPOs globally versus over 46,000 M&A deals that same year.

When a company is acquired, the process can vary for shareholders depending on the deal that is struck between the two participating companies. Shareholders could have their equity converted from shares of the company being acquired to shares of the new company, shareholders could be paid out with cash or there could be a combination of both.

Let’s assume Company X is acquired by Company Y for $750,000,000 for cash. At a $750M acquisition price the price per share of all outstanding shares would be $18.75 a share ($750M/40M shares). Because $18.75 is higher than any of the preferred rounds' original issue prices, all the preferred shares would convert to common stock. The fully converted common stock would then share pro rata in the $750M at $18.75 a share.

Now, if instead Company X was acquired for $350,000,000 in an all-cash acquisition, the distribution to preferred shareholders would be very different. When dividing $350M by the 40M shares outstanding the price per share comes out to $8.75. In this example the Series C Preferred investors acquired shares at $12.50/share. Because the Series C Preferred original issue price is above $8.75, the Series C shareholders would choose to not convert into common stock and would receive their original investment back at $12.50 a share, the original issue price of the Series C. The Series C shareholders would receive a total of $187.5M of the acquisition payout, leaving $162.5M for remaining shareholders. This $162.5M would then be divided amongst the remaining 25M shares outstanding, resulting in a liquidation price per share of $6.50 for remaining shareholders. This price per share is higher than the original issue price of the Series B Preferred shares and the Series A Preferred shares, meaning investors in both of these funding rounds made money on their investment. Due to this, these early stage shareholders would convert to common stock and share pro rata with the other common stock shareholders at $6.50 a share.

When a Company Goes Public

The more widely known type of liquidation event is an Initial Public Offering (IPO) which is the listing of a previously private company on a publicly traded exchange like NASDAQ or the New York Stock Exchange. This allows public market investors to purchase shares of the company and enables the shares to actively trade on the open market. Like an acquisition or merger, the process of taking a private company public can become complex depending on the underlying ownership structure of the company.

Often there are terms within a company’s Certificate of Incorporation (COI), if U.S. based, which protect shareholders from a company going public too early. These terms require the company to wait until the company reaches a certain valuation or common stock price per share. The company must also determine how any outstanding warrants, options and restricted stock units (RSUs) will be handled. Typically, these equity vehicles will convert to common stock during an IPO unless there is another agreement made between the company and the holders of these vehicles. Preferred shares also typically convert to common stock automatically at the time of an IPO.

Another restriction private company shareholders should be aware of is the IPO lock-up period which can range from 90 to 180 days and prevents shareholders, whether institutions or accredited investors, from selling their pre-IPO stock. This lock up period is to prevent company insiders from selling shares during the first few months of the company trading. This attempts to prevent large swings in the company’s stock price from early investors, employees and founders offloading their shares.

Using Company X, we can demonstrate the impact of an IPO for shareholders in the company. We will assume that the company has no debt, RSUs or outstanding warrants for the company. Company X decides to list for its Initial Public Offering by issuing 30M shares of common stock at $20 a share on January 1st, 2024. With the issuance of the 30M new shares of common stock and the conversion of preferred shares to common, the company would now have 70M shares of common stock outstanding post-IPO. At $20 a share the company’s market capitalization would equal $1.4B.

The company also has a 90 day lock up period for previous shareholders. At the 90-day mark, March 31st, Company X’s shares are trading at $18.00 a share. At this point all previous shareholders would have seen a positive gain in stock price and can now decide if they want to sell the shares or hold onto them in hopes for continued appreciation in the stock.

These examples outline some of the common exit options for private companies and the impact on shareholders on a company's cap table. However, these examples outline “vanilla” transactions, with minimal complexity to illustrate the flow of capital. Cap table provisions can run the gamut, and often include more complex elements like additional protective provisions, differing liquidation preferences, multiple conversion rates and various other contingencies and triggers. It’s important to keep in mind that these factors, along with other debt financing can add further complexity to the overall returns available to common equity holders during an exit event.

Understanding the impact of various exit scenarios as a private company investor is a key part in performing due diligence on a company before buying pre-IPO shares. That is why EquityZen's secondary marketplace prepares cap tables for all Standard Deals to help investors make informed decisions. Interested in analyzing the cap table of a specific private company? Search the company on EquityZen’s platform and can request a cap table.

![]()

Interested in browsing the private company investment opportunities available on EquityZen's marketplace?

Disclaimer: A lack of publicly available and verifiable information can materially impact the accuracy of information provided, including without limitation, estimates relating to the valuation and capitalization of companies subject to investment.

Not all pre-IPO companies will go public or be acquired, and not all IPOs or acquisitions are or will become successful investments. There are inherent risks in pre-IPO investments, including the risk of loss of the entire investment, illiquidity, and fluctuations in value and returns. Investors must be able to afford the loss of their entire investment

Join Investors and Shareholders Exploring the Private Markets Today