In this article

A Historic Start to 2026

The first quarter of 2026 showed continued investor demand for innovation, despite significant market volatility. From the capture of Maduro in Venezuela to the ongoing war in Iran, geopolitical conflicts have taken center stage. These events have been coupled with a weakening dollar, cries of a “Saaspocalpyse” in February and broader concerns of recession, leading to a shaky market environment. All major indices traded down year-to-date at the close of the quarter.

The volatility in the public markets, however, has not stopped the breakneck pace of funding and innovation within the private markets. Investors poured a record-breaking $300 billion into 6,000 startups globally in the quarter, an increase of over 150% quarter over quarter. However, the narrative in Q1 2026 has been dominated by capital concentration at the very top. OpenAI closed its $122 billion round at the end of the quarter, becoming the largest VC round of all time. In fact, four of the five largest venture rounds ever1 recorded closed in Q1 2026, including OpenAI and Waymo ($16 billion), collectively raising $188 billion and accounting for 65% of all global venture investment in the quarter.

While the broader venture ecosystem continues to navigate a bifurcated market of tight fundraising for emerging managers (with a mere $58.4 billion of new commitments2 closed globally in Q1) and massive mega-rounds for AI leaders, investor appetite for category-defining technology has never been more intense. AI completely shattered records last quarter, capturing over 80% of total global venture funding. Beyond market hype, this unprecedented level of funding is largely driven by the staggering capital costs required to power the AI boom: from chips to data centers and AI talent.

Such capital concentration pushed late-stage funding to $246.6 billion, up over 205% year-over-year1, while the top five deals in the US alone exceeded the entire non-US deal value for the quarter. The capital boom in the late-stage market exemplifies the growing demand for access to potential near-term IPO contenders, something we’ve seen echoed in EquityZen’s own data. Comparatively, early-stage funding was up 41% year-over-year.

Many expected 2026 to be a breakout year for IPOs. However, only twenty-one venture backed unicorns1 went public in Q1, including companies like BitGo and EquipmentShare. Meanwhile, several companies, like Motive, have tabled their plans, choosing to wait for more market certainty before ringing the bell. This landscape could shift dramatically, as several centacorn companies have signaled public market intentions. Together, these companies could clear $2.5 trillion in market value upon their listings, which would exceed the total global exit value generated since 20222.

The M&A market was more active, with Q1 being the third highest quarter1 since 2022. However, this activity was also highly concentrated. According to Pitchbook data, when you strip out mega-mergers, Q1 global exit value was just $131.5 billion, the lowest total since Q2 of last year. This leaves a backlog of over 1,300 unicorn companies worth a collective $6.4T3 continuing to grow in the private markets.

So how did this macro landscape translate to activity in the private secondary market? Here we analyzed thousands of data points from EquityZen’s platform to break down the top trends driving investor activity.

Investor Interest Accelerates

While public market investors await several highly anticipated IPOs, private market investors are investing now via the private secondary market. Against this backdrop of mega-rounds and looming IPOs, investor interest on the EquityZen platform remained robust in Q1. Following a strong finish to last year, investor indications of interest increased 24.9% throughout the quarter4. Specifically, we saw a surge in demand from investors looking to invest in AI companies. This likely comes as no surprise, given the robust primary funding activity within Q1 for AI leaders.

AI Dominates, Hard Tech Gains Ground

Artificial Intelligence retained its crown as the #1 most sought-after sector on EquityZen in Q1, a position it has held uninterrupted for over two years. However, the rest of the industry leaderboard saw a dramatic reshuffling that heavily favors frontier technology and physical infrastructure.

Aerospace trended up to the #2 spot, while Manufacturing climbed steadily to #4 (from #6 in Q4 2025), illustrating a shift toward “hard tech”. Meanwhile, traditional software and financial technology categories continue to cede ground to these capital-intensive sectors with Fintech dropping to #5. We also saw a slight rebound for SaaS, which ticked up to #6.

While sectors like National Security and Advanced Materials saw a dip this quarter after a strong late-2025 run, the overall picture is clear: EquityZen investors are balancing their massive appetite for AI with a focus on companies building for the physical world and the infrastructure required to fuel tech’s biggest advancements.

Climbing the Ranks: Hard Tech and Infrastructure Surge

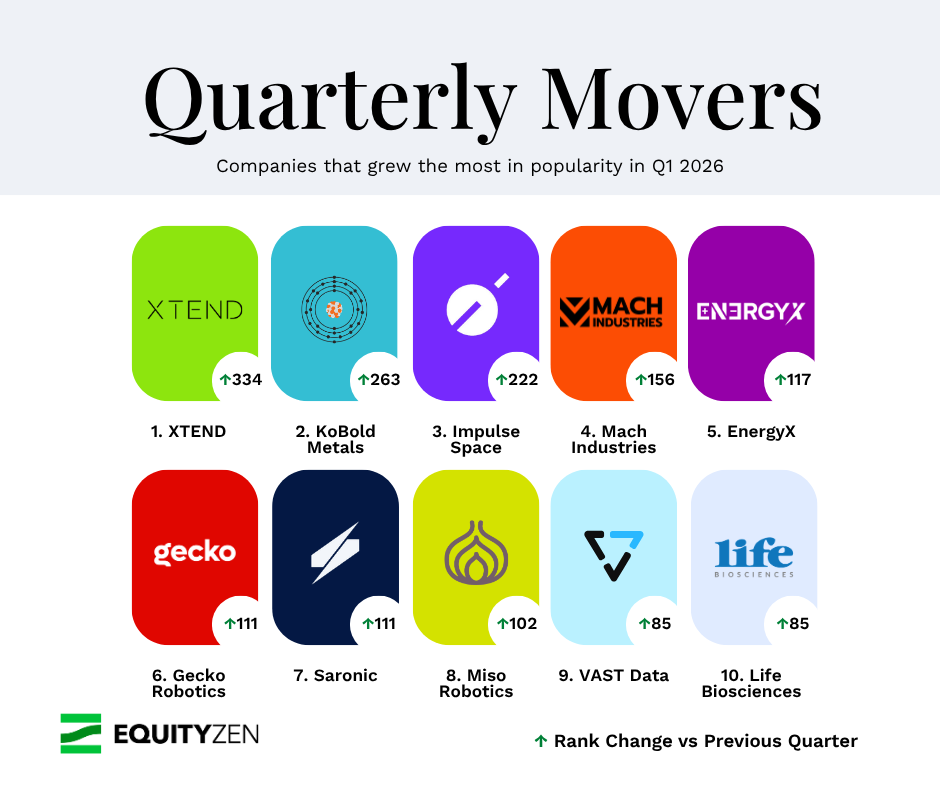

EquityZen’s "Quarterly Movers", which tracks the companies with the largest jump in investor popularity rank quarter over quarter, reveals where the next wave of investor demand is growing. In Q1 2026, the data points to a notable surge in interest for physical infrastructure, defense tech, and the energy supply chain:

- The Defense and Robotics Renaissance: The biggest leaps in popularity belonged to companies building intelligent machines for the physical world. XTEND (+334 spots), which develops AI-driven drone systems, led in popularity growth. Defense tech innovators like aerial systems and hardware company Mach Industries (+156) and autonomous vessel manufacturer Saronic (+111) saw massive interest spikes, underscoring the growing mainstream appeal of national security technology. Commercial robotics also surged, driven by infrastructure inspector Gecko Robotics (+111) and food-tech automation company Miso Robotics (+102).

- The Energy and Resource Boom: As the AI revolution demands unprecedented power, investors are aggressively targeting the raw materials supply chain. KoBold Metals (+263), which uses AI for mineral exploration, was the second-highest mover of the quarter. Lithium battery maker EnergyX (+117) also saw a top-five surge in popularity, signaling that investors are hunting for clean energy and mining innovation.

- Space and AI "Picks and Shovels": Riding massive pre-IPO momentum, space transportation company Impulse Space (+222) shot up the rankings. Meanwhile, as foundation AI models mature, investors are seeking out the critical backend infrastructure supporting them, evidenced by a major ranking jump for AI data storage platform VAST Data (+85).

Shrinking Discounts: The Return of the Premium

The era of deep secondary market discounts appears to be ending as investor demand heats up. In a dramatic shift from the previous year, the average company on EquityZen traded at an 8% discount to its last round in Q1 2026. As the chart below illustrates, this is a massive contraction from the 29% average discount seen at the end of 2025, and a far cry from the 49% discounts seen at the start of 2024.

Furthermore, buyers are increasingly willing to pay up for high-conviction assets. In Q1 2026, 34% of secondary trades on EquityZen executed at a premium to the company's last primary funding round, a significant jump from just 19% at the end of 2025. This steep drop in overall discounts and the rapid rise in premium transactions underscores the intense competition among investors trying to secure allocations in top-tier pre-IPO companies before they hit the public markets. As the IPO window threatens to open wider, the window for deep secondary value plays is simultaneously closing.

A closer look at sector-specific data reveals that valuations are not a one-size-fits-all story. The surge in premium transactions is highly concentrated in frontier and hard tech. Industrials and Traditional Tech (Software/Hardware) led the pack, with 67% of companies in both sectors trading at a premium in Q1. Artificial intelligence, machine learning & natural language processing followed closely with 53% of companies commanding a premium, while Emerging Energy saw an even 50/50 split. Conversely, sectors that dominated the previous cycle are still providing deep value opportunities. Consumer and Lifestyle Tech, Enterprise SaaS, FinTech, and Health Care saw all of their companies trading at a discount. This stark contrast highlights that while the overall market discount is shrinking, investors remain highly selective, paying top dollar for physical infrastructure, AI, and energy, while demanding discounts for traditional software and consumer plays.

Hunger for the Heavyweights

Mega-cap companies didn’t just attract the most attention this quarter; EquityZen data reveals a fascinating reversal in actual trading behavior. In Q1, 57% of transactions occurred in companies valued at greater than $20 billion, a notable change from recent quarters, where we saw growing transactions amongst younger companies. There are two key factors driving this. First, the most high-profile private companies are reaching higher valuations than ever within the private markets. Decacorn status has become a new normal as valuations continue to grow. Second, investors are keenly focused on the companies that may be near-term IPO contenders. This is where secondaries can become attractive opportunities to achieve returns more quickly than earlier stage primary investments.

Looking Ahead

The first quarter of 2026 set a blistering pace for the private markets, defying broader market volatility. Record-breaking AI mega-rounds and the potential for an IPO resurgence in the back half of 2026 have brought unprecedented attention to late-stage venture capital.

As EquityZen's proprietary data reveals, this capital concentration at the top is fundamentally reshaping secondary market dynamics. We are witnessing a decisive flight to scale, with more investors aggressively targeting heavyweights. This was exemplified by the majority of transaction volume shifting to decacorns valued at over $20 billion. Simultaneously, we’re seeing a sharp bifurcation in valuations. While highly sought-after frontier tech, aerospace, and AI companies are now frequently commanding premiums, disciplined investors can still find deep value and steep discounts in traditional enterprise SaaS, fintech, and consumer sectors.

As the pre-IPO landscape continues to evolve, given the breakneck speed of innovation, understanding these nuances and securing access to unique investment opportunities remains the ultimate competitive advantage.

Join Investors and Shareholders Exploring the Private Markets Today

-1.png?width=812&height=446&name=Q1%20(1)-1.png)