In this article

Ten years ago, just as EquityZen was getting started, Eileen Lee of Cowboy Ventures coined the term “Unicorn” to describe private companies valued at over $1 billion. Since then, the term has become ubiquitous in the venture market, and as valuations grew over time, the Unicorn status lost some of its luster. After all, in 2013 only 39 unicorns existed while today, after a decade of venture-fueled growth, there are an estimated 1,200 Unicorns worth an aggregate $3.7 trillion. But the market has changed. Just last week the fintech Bolt announced a share buyback at a mere $300 million valuation, a far cry from the $11 billion valuation at which they last raised capital, losing their Unicorn status. Over 400 Unicorns have not raised funding since 2021, which begs the question, how many of these companies are still true Unicorns? Here we breakdown our own analysis of the Unicorn market, powered by data from EquityZen’s platform.

Unicorns have fallen in the secondary market

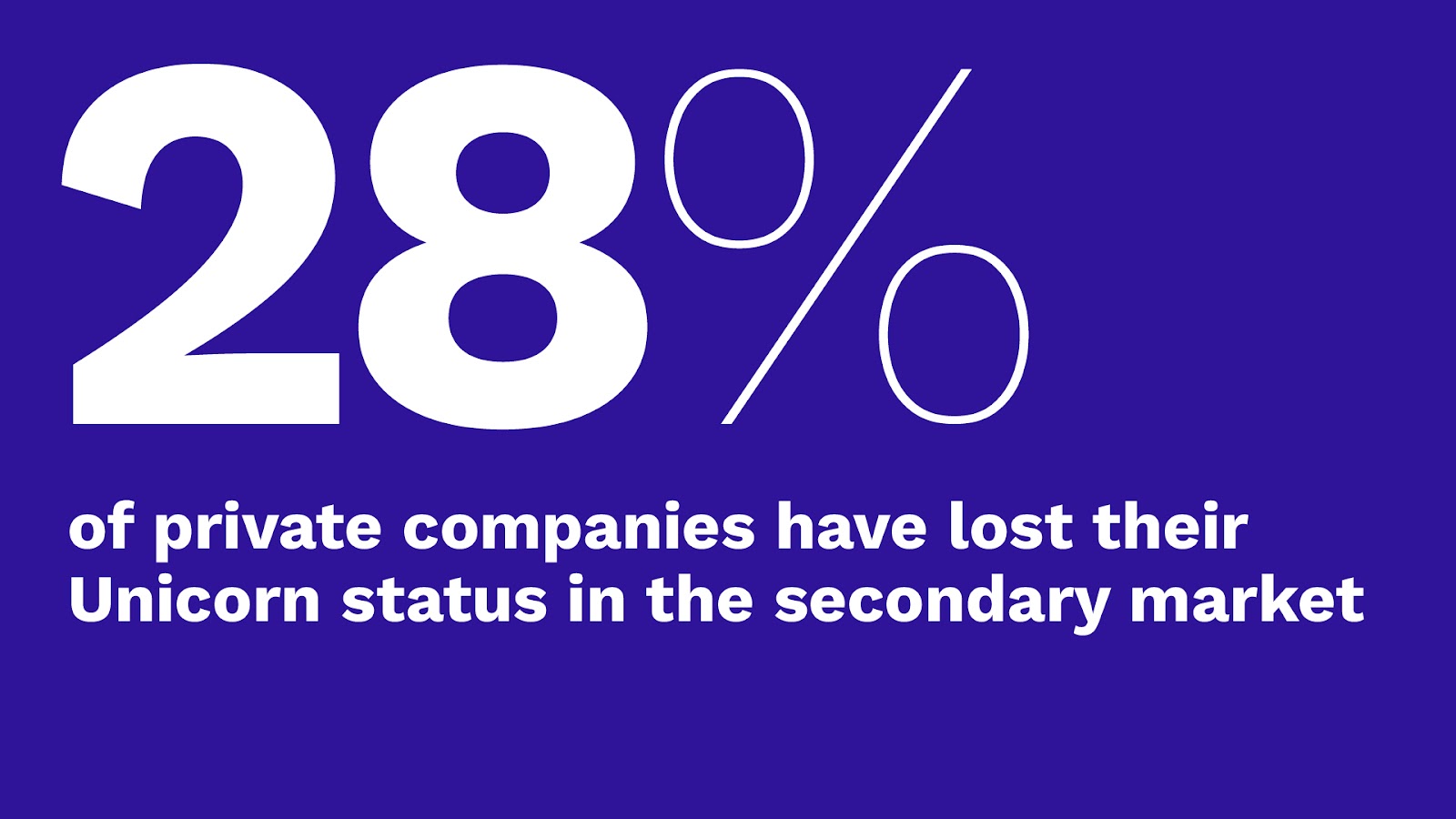

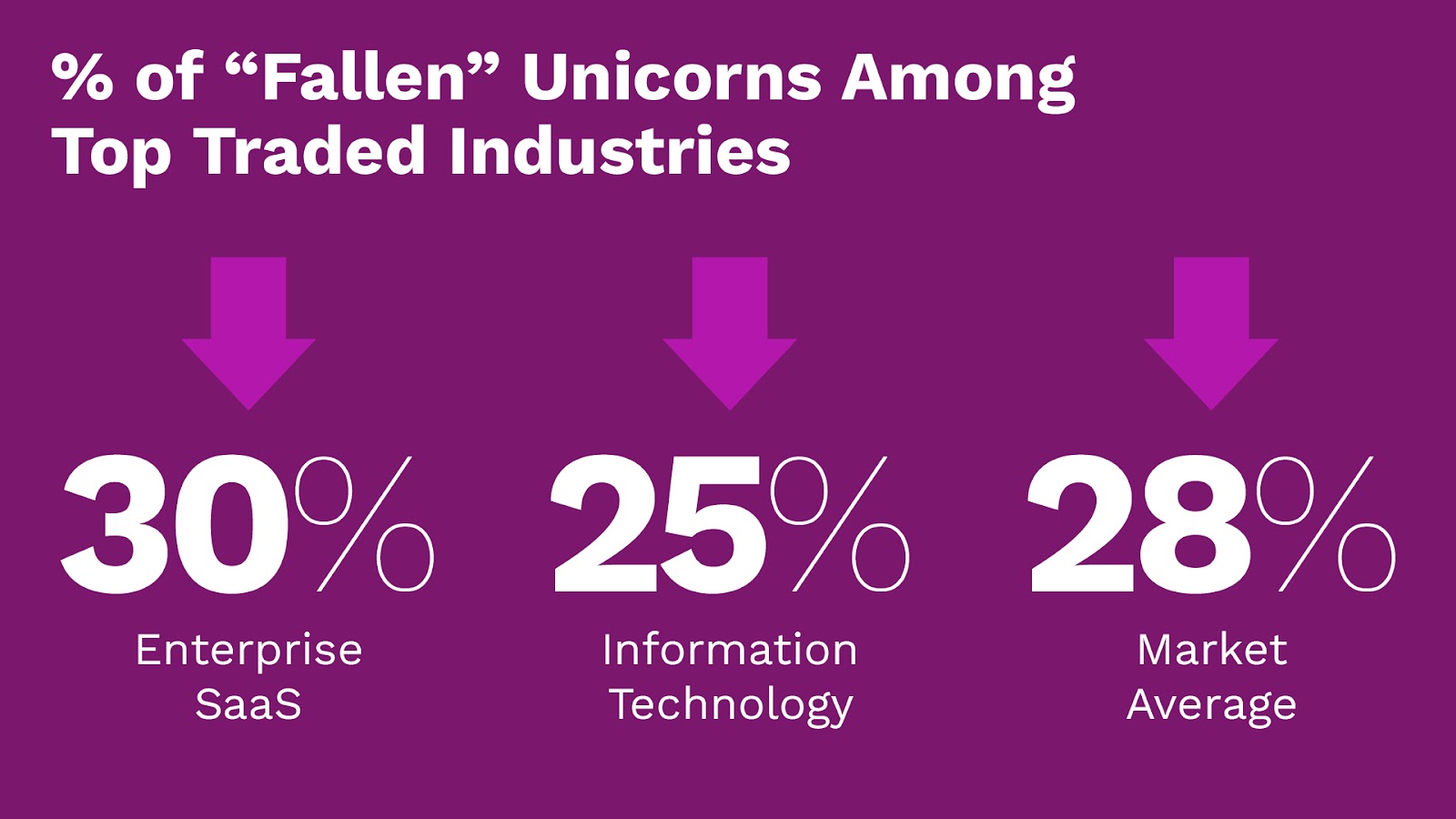

To cut to the chase, many Unicorns have fallen. Of the Unicorn companies in which EquityZen conducted secondary transactions over the past 2 years, 28%1 are trading at valuations less than $1B, thereby losing their Unicorn status. If you were to extrapolate this to the global Unicorn number this would mean that over 330 Unicorns have fallen. Perhaps this is not too surprising as more companies have had down rounds publicly covered in the news, while others have gone unreported. In fact, 17% of all VC investing rounds in Q3 of last year were down rounds versus 5% of funding rounds in 2021. Last year Tonal raised money at a reported $550m valuation, about one-third of its 2021 valuation. Instacart’s IPO was itself a down round, with an IPO price that was 74% less than their last private funding round of $39 billion. In aggregate, Pitchbook observed that 44% of late stage funding rounds were flat or down in 2023. As more private and public fundraises take place this year, alongside a hopeful increase in M&A activity, down rounds will continue to become more normalized and as this happens we will see more Unicorns formally lose their title.

A new normal

So is the loss of unicorn status a death blow? Certainly not. Just as public equities adjusted to a normalization of multiples, the same process is happening in the private markets, leading some Unicorns to lose their status, at least temporarily. The average public technology company is currently trading at a 4.6x sales multiple on the NASDAQ4. Meanwhile some Unicorn companies raised capital at upwards of 100x multiples in the height of the market. Investors now also have less appetite for unprofitable companies than during the startup friendly, ZIRP-fueled era of “growth at all costs” and this valuation correction is a healthy adjustment. It is just a matter of time before this is reflected in new valuation marks from primary funding rounds.

This need for multiple corrections amidst a different macroeconomic environment with changing investor expectations puts some Unicorn companies in a difficult situation. According to Pitchbook, less than 25% of U.S.-based Unicorns are profitable. The others are burning cash at a time when venture capitalists are more weary to pump additional capital into existing investments and are instead looking for exits and liquidity. Meanwhile, non-traditional investors who had entered the venture market in its height have now exited. This means that these unprofitable private companies are likely simultaneously working towards profitability, while attempting to raise additional capital in a tough funding environment. A quiet M&A market, partially driven by antitrust regulations, have made this exit avenue harder for companies too. These unprofitable Unicorns are at risk of officially losing their horns and the herd will inevitably thin. If these companies are able to raise funding it will likely be at a significant discount to the last round of funding raised, potentially at a valuation of less than $1 billion. These funding events will likely bring the number of real Unicorns closer to the number we’re seeing on EquityZen’s platform.

![]()

Interested in exploring the private companies trading on EquityZen's marketplace?

Deal activity will drive a valuation reset

One of the benefits of private investments is that they are typically shielded from the volatility that comes with daily marks to market. In the current market environment this delay in marks has been further extended. According to Pitchbook, the median time between funding rounds has widened to 1.78 years, the longest time observed in over a decade. Yet, the long periods of time between formal funding rounds can actually hinder market activity, with investors and private companies both unsure of a fair market price and therefore less likely to close deals. We saw this in 2022 and early 2023 as the bid-ask spread between buyers and sellers on EquityZen’s platform remained wide. As the market adjusts to the new normal, the bid-ask spread has narrowed which has allowed more transactions to take place in the secondary market. Because of this, the secondary market can help drive primary activity by providing up-to-date data on supply, demand and valuations from both a market and company-specific perspective.

As more of these updated marks become publicized, down rounds will become more normalized, allowing a broader reset of valuations for all companies, not just Unicorns. After all, it’s important to note that down rounds are completely normal in the public markets. Public companies can trade down for days, months, or even years. While down markets typically come with volatility and risk, savvy investors in both the public and private markets know that these periods of valuation decreases can provide attractive buying opportunities for those who believe there is future growth to be had. Perhaps this era will help eliminate some of the stigma associated with these rounds in the private markets and the heightened obsession with valuations, and specifically Unicorn valuations, that we see in the private market.

The term Unicorn may have lost its elusive magic and there are certainly less “real” Unicorns than paper Unicorns based solely on the latest primary funding round. Yet, market pundits expect this year to be a more normal one for both IPOs and M&A. While some late stage companies will inevitably become Unicorpses, as more late stage companies continue their shift to profitability we’ll start to see new leaders emerge who are continuing to grow and innovate within their respective industries. The market’s obsession with the term Unicorns over the past decade paints a picture of a market focused solely on valuation growth. So maybe it's time to redefine the term, or come up with a new one to recognize the emerging private companies leading the way in this new market paradigm. Perhaps they will be the Phoenixes rising from the ashes.

![]()

Interested in exploring the private companies trading on EquityZen's marketplace?

Sources:

- EquityZen data, as of 2/8/2024

- CAIS. September 2022

- EquityZen data, as of 2/8/2024

- YCharts. As of February 6, 2024

- EquityZen data, as of 2/13/2024

Join Investors and Shareholders Exploring the Private Markets Today